“Although export volumes have declined year over year, current steel production is also lower compared to last year.

Therefore, there isn’t much supply pressure in either the steel export market or the domestic market, which can provide some support for currently rising steel prices,” said another trader.

The daily pig iron and crude steel output at China Iron and Steel Association member mills averaged 1.85 million mt and 2.036 million mt over April 21-30, about 5.6% and 7.5% lower than in the same period of last year, CISA’s latest data showed.

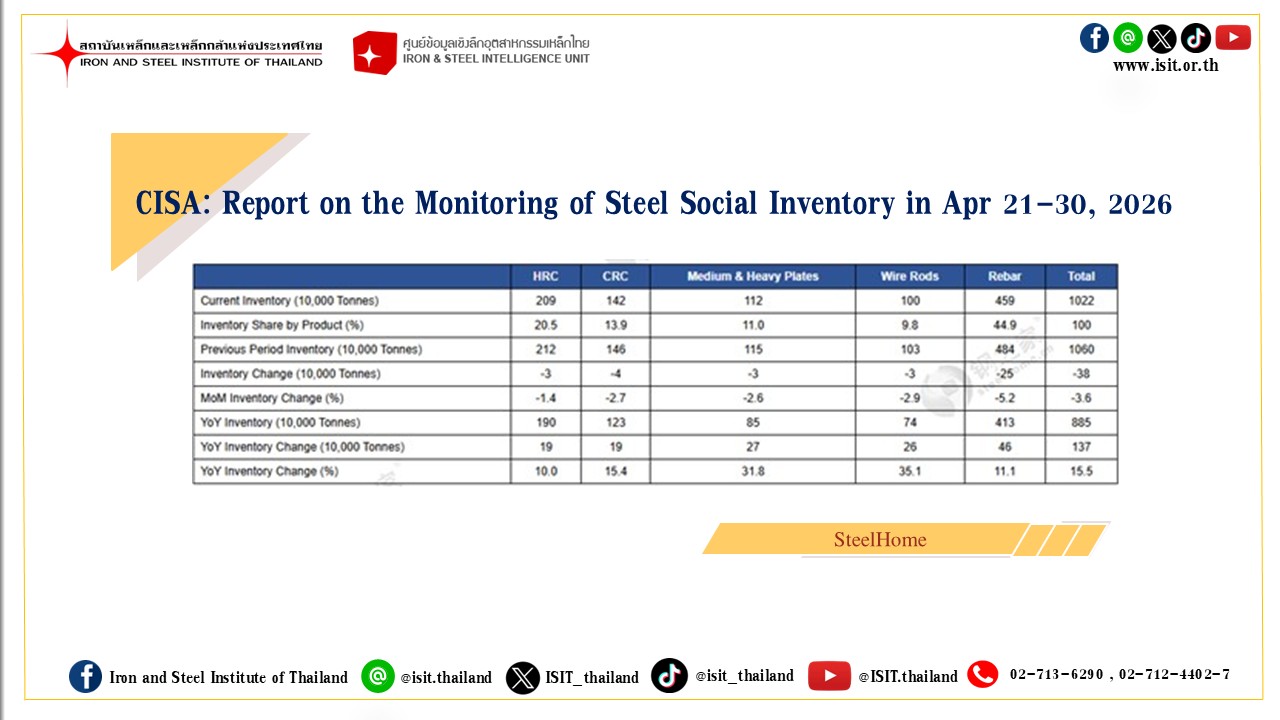

The finished steel inventories at mills and major spot markets monitored by CISA reached 25.65 million mt as of April 30, down 8.3% from end-March, but still 6.3% higher year over year, CISA data showed.

While domestic demand had remained sluggish overall, steel prices had risen rapidly recently, a mill source said. This is likely because steel production remained in a year-over-year decline, and steel exports were still relatively strong, they added.

However, some export traders said the recent rise in steel prices had already led to a pullback in export orders for June shipments.

Platts, part of S&P Global Energy, assessed domestic hot rolled coil and rebar prices at a respective Yuan 3,520/mt ($518/mt) and Yuan 3,330/mt May 11, both up 7% from April 15.

Platts assessed SS400 HRC and BS500B-grade rebar at $506/ mt FOB China and $505/mt FOB China on May 11, up 5% and 4%, respectively, from April 15.